Best Credit Cards for Beginners USA 2026: The Complete Guide to Building Credit From Zero

Imagine this: You just moved to the United States — or maybe you just turned 18. You go to rent an apartment, apply for a car loan, or even try to sign up for a simple phone plan, and you hit the same invisible wall every time.

“We couldn’t approve you. Insufficient credit history.”

It’s one of the most frustrating financial Catch-22s in America: you need credit to get credit. Nobody hands you a financial reputation — you have to build one, brick by brick. And the foundation of that reputation? Your very first credit card.

Choosing the right first credit card is not a small decision. The card you pick in 2026 will influence the credit score that follows you for decades — affecting your ability to rent an apartment, finance a car, qualify for a mortgage, and even land certain jobs. This guide was written for you: the student, the new immigrant, the recent graduate, the first-timer who deserves a fair shot at the American financial system.

Let’s cut through the noise and get you started on the right foot.

What Is a Credit Card & How It Works in the USA

A credit card is a short-term revolving loan issued by a bank or financial institution. When you make a purchase, the card issuer pays the merchant on your behalf. You then repay the issuer — ideally in full each month.

Here’s how the U.S. credit system works in practice:

- Billing cycle: Typically 30 days. At the end of each cycle, you receive a statement showing your balance.

- Due date: You have until the payment due date to pay. Pay the full balance and you owe zero interest.

- Minimum payment: If you can’t pay in full, you can pay a minimum (usually $25 or 1–2% of the balance) — but the remainder carries interest, often at 20–29% APR.

- Credit limit: The maximum amount you’re allowed to borrow. For beginners, this is usually $200–$1,000.

- Credit bureaus: Every month, your card issuer reports your payment behavior to the three major bureaus — Experian, Equifax, and TransUnion. This is how your credit history gets built.

The key rule for beginners: Use the card. Pay it off. Repeat. This simple loop — over months and years — is how you build a powerful credit profile.

Why Your First Credit Card Is So Important in 2026

Your FICO credit score is a three-digit number ranging from 300 to 850. It tells lenders, landlords, and even some employers how financially reliable you are. As of early 2026, the average FICO Score in the U.S. sits at approximately 715 — solidly in the “good” range. But getting there from zero takes time, strategy, and the right starting card.

Here’s why your first card choice in 2026 matters more than ever:

1. It starts your credit clock. The length of your credit history accounts for 15% of your FICO score. The sooner you open an account, the longer that history grows — which benefits you for life.

2. It sets your habits. The patterns you build now — paying on time, keeping balances low — become automatic. Studies show that people who start with responsible credit habits rarely abandon them.

3. It unlocks your financial future. Without a credit history, you can’t qualify for most mortgages, personal loans, or premium rewards cards. Your starter card is the ladder rung that makes everything else reachable.

4. New 2026 developments help beginners. Equifax, Experian, and TransUnion have removed most paid medical collections from credit reports, and medical debts under $500 no longer appear — giving millions of consumers a cleaner credit starting point. Additionally, tools like Experian Boost now allow you to report rent, utility, and streaming payments to the bureaus, accelerating early credit-building significantly.

Secured vs. Unsecured Credit Cards: A Beginner’s Guide

Before you apply for anything, you need to understand this fundamental distinction.

Secured Credit Cards

A secured card requires you to deposit money upfront — typically $200 to $500 — which becomes your credit limit. The bank holds this as collateral. If you stop paying, they keep the deposit.

Why this exists: It reduces the lender’s risk, which means they’ll approve people with no credit history or poor credit.

The upside: Using a secured credit card responsibly can help you build up a history of good credit management, increasing your score over time and opening the door to a wider range of credit products in the future.

The upgrade path: Most secured cards automatically review your account after 6–12 months. If you’ve paid on time and kept your balance low, many issuers will refund your deposit and upgrade you to an unsecured card.

Unsecured Credit Cards

No deposit required. Approval is based on your creditworthiness — income, existing debts, and credit history. For true beginners, unsecured approvals are harder but not impossible. Cards like the Chase Freedom Rise℠ and Petal 2 Visa are designed specifically to approve people with thin or no credit files.

Which Should You Choose?

| Situation | Recommended Type |

|---|---|

| Zero credit history | Secured (most reliable) |

| Student with .edu email | Student unsecured card |

| Recent immigrant, no SSN | Zolve or secured card |

| Some income, no credit | Unsecured beginner card |

| Credit score under 580 | Secured card |

Top 7 Best Credit Cards for Beginners in the USA (2026)

🏆 #1 — Discover it® Secured Credit Card

Best for: Overall beginners with no credit history

| Feature | Detail |

|---|---|

| Annual Fee | $0 |

| Security Deposit | $200 minimum (refundable) |

| APR | 27.24% variable |

| Minimum Credit Score | None required |

Key Features: The Discover it® Secured Credit Card is a good option for beginners with no credit because it is inexpensive to own, offers great rewards, prevents you from overspending, and can help you build credit with responsible use. It offers 2% cash back at gas stations and restaurants on up to $1,000 in combined purchases each quarter, and 1% on everything else. At the end of your first year, Discover automatically matches every dollar of cash back you earn — doubling your rewards through their Cashback Match promotion.

Discover also reports to all three major credit bureaus monthly and reviews your account for an upgrade to an unsecured card in as little as 7 months.

Pros:

- No annual fee — rare for a secured card

- Cashback Match in year one is genuinely unmatched

- Automatic upgrade review at 7 months

- No minimum credit score required

Cons:

- $200 deposit required upfront

- Discover isn’t accepted everywhere internationally

Who should use it: Anyone starting from absolute zero. This is the gold standard of beginner cards in 2026.

#2 — Chase Freedom Rise℠

Best for: Unsecured beginners who want rewards from day one

| Feature | Detail |

|---|---|

| Annual Fee | $0 |

| Security Deposit | None |

| APR | 25.99% variable |

| Minimum Credit Score | None required |

Key Features: The Chase Freedom Rise® has everything you want to see in a credit card meant for beginners: a low barrier to approval, a $0 annual fee, solid rewards on everything you buy, and a potential upgrade path to any number of other excellent credit cards in the Chase portfolio. There’s no annual fee to worry about, and since it’s an unsecured credit card, there’s no upfront deposit required either. You don’t even need a credit history to qualify. On top of that, the card earns a flat 1.5% cash back on all purchases, which is competitive with many cards that have more stringent credit requirements.

Approval tip: Having a Chase checking or savings account with a positive balance significantly boosts your approval odds — even with zero credit history.

Pros:

- No deposit needed — zero barrier to entry

- 1.5% flat cash back is excellent for a no-credit card

- Upgrade path to Chase Freedom Flex or Chase Sapphire Preferred

- Reports to all three bureaus

Cons:

- Better odds if you already bank with Chase

- No intro 0% APR offer

Who should use it: Beginners who want a real rewards card without tying up cash in a deposit, especially those already banking with Chase.

#3 — Capital One Platinum Credit Card

Best for: Building unsecured credit with no frills

| Feature | Detail |

|---|---|

| Annual Fee | $0 |

| Security Deposit | None |

| APR | 29.99% variable |

| Minimum Credit Score | No credit / limited credit |

Key Features: No deposit, no annual fee, no rewards — but that’s the point. The Capital One Platinum is purely designed to get you approved and start building. Capital One reviews your account for a higher credit limit after just 6 months of responsible use, which directly improves your credit utilization ratio and boosts your score.

Pros:

- Instant consideration for credit limit increase at 6 months

- No deposit required

- Widely accepted on Mastercard network

- Free CreditWise monitoring included

Cons:

- No rewards of any kind

- High APR — don’t carry a balance

Who should use it: Those who want simplicity. No rewards confusion — just a clean, straightforward card to build credit.

#4 — Discover it® Student Cash Back

Best for: College students with no credit history

| Feature | Detail |

|---|---|

| Annual Fee | $0 |

| Security Deposit | None |

| APR | 17.24%–26.24% variable |

| Eligibility | Must be a college student |

Key Features: A student credit card is a credit card designed for students who haven’t built up a credit history yet. They’re often unsecured, easy to qualify for, and typically come with no annual fees. The Discover it Student Cash Back earns 5% cash back in rotating quarterly categories (like Amazon, restaurants, and gas stations) and 1% on everything else. It also includes the first-year Cashback Match.

There’s also a $20 Good Grade Reward each year you maintain a 3.0 GPA — a nice nod to responsible students.

Pros:

- No credit history required

- Among the best rewards of any student card

- 0% intro APR for 6 months on purchases

- Good Grade Reward ($20/year with 3.0 GPA)

Cons:

- Only available to enrolled college students

- Rotating categories require activation each quarter

Who should use it: Any college student in the U.S. This is the strongest student card available right now.

#5 — Petal® 2 “Cash Back, No Fees” Visa® Credit Card

Best for: Immigrants and people with no credit file who have income

| Feature | Detail |

|---|---|

| Annual Fee | $0 |

| Security Deposit | None |

| APR | 18.24%–31.99% variable |

| Minimum Credit Score | None — uses bank data |

Key Features: The Petal 2 is genuinely innovative. Instead of using a traditional credit score, Petal reviews your bank account data — income, spending, and savings patterns — to evaluate your creditworthiness. This makes it ideal for immigrants, international students, and anyone with a “thin file.”

The card earns 1% to 1.5% cash back on purchases as you pay on time — scaling up your reward rate as you prove your reliability. No late fees, no foreign transaction fees, no deposit needed.

Pros:

- Approves based on income, not credit history

- No fees of any kind

- Credit limit up to $10,000 — unusually high for a beginner card

- Rewards increase over time with on-time payments

Cons:

- Requires linking your bank account during application

- APR can be high on the upper end

Who should use it: New immigrants, international students, and anyone whose credit file doesn’t reflect their actual financial responsibility.

#6 — Capital One Quicksilver Secured Credit Card

Best for: Secured card with unlimited cash back

| Feature | Detail |

|---|---|

| Annual Fee | $0 |

| Security Deposit | $200 minimum |

| APR | 29.99% variable |

| Minimum Credit Score | No credit required |

Key Features: Most secured cards offer no rewards. The Capital One Quicksilver Secured breaks that mold by offering unlimited 1.5% cash back on every purchase — the same rate as many premium unsecured cards. Combined with Capital One’s credit limit review at 6 months and upgrade path to the unsecured Quicksilver, this card offers both immediate value and long-term progression.

Pros:

- 1.5% cash back — extremely rare on secured cards

- Upgrade path to unsecured Quicksilver

- Reports to all three bureaus

- No penalty APR

Cons:

- $200 deposit required

- High APR — pay in full monthly

Who should use it: Beginners who want a secured card but refuse to sacrifice rewards while building credit.

#7 — Bank of America® Customized Cash Rewards Credit Card

Best for: Beginners who already bank with Bank of America

| Feature | Detail |

|---|---|

| Annual Fee | $0 |

| Security Deposit | None |

| APR | 18.24%–28.24% variable |

| Minimum Credit Score | 670+ recommended |

Key Features: This card is more accessible if you already have a Bank of America checking or savings account. It earns 3% cash back in a category you choose (gas, online shopping, dining, travel, drug stores, or home improvement), 2% at grocery stores and wholesale clubs, and 1% on everything else. There’s also a $200 online cash rewards bonus after spending $1,000 in the first 90 days.

Pros:

- Excellent rewards structure for everyday categories

- $200 welcome bonus

- Preferred Rewards members get up to 75% more cash back

- 0% intro APR for 15 billing cycles on purchases

Cons:

- Generally requires fair-to-good credit — harder for absolute beginners

- Best value locked behind Bank of America relationship

Who should use it: Beginners who’ve spent 6–12 months building credit with a starter card and are ready to upgrade to something with real earning power.

Quick Comparison Table: Top 7 Beginner Credit Cards

| Card | Annual Fee | Deposit | Rewards | Best For |

|---|---|---|---|---|

| Discover it® Secured | $0 | $200 | 2%/1% + Match | Overall best beginner |

| Chase Freedom Rise℠ | $0 | None | 1.5% flat | No deposit + rewards |

| Capital One Platinum | $0 | None | None | Pure credit building |

| Discover it® Student | $0 | None | 5%/1% rotating | College students |

| Petal® 2 Visa | $0 | None | 1–1.5% | Immigrants / thin file |

| Capital One Quicksilver Secured | $0 | $200 | 1.5% flat | Secured + rewards |

| BofA Customized Cash | $0 | None | 3%/2%/1% | After 6 months building |

How to Choose the Best Beginner Credit Card for You

Not every card is right for every person. Use this decision framework:

- No credit history, want no deposit? → Chase Freedom Rise℠ or Petal 2

- No credit history, OK with deposit? → Discover it® Secured (best overall)

- Currently enrolled in college? → Discover it® Student Cash Back (no contest)

- Immigrant or no Social Security Number? → Petal 2 or Zolve Classic

- Already bank with Capital One? → Capital One Quicksilver Secured

- Want the simplest possible card? → Capital One Platinum

- Built some credit and ready to upgrade? → Bank of America Customized Cash

Key factors to weigh before applying:

- Does it report to all three bureaus? (Non-negotiable — all 7 above do)

- What is the annual fee? (Should be $0 for any beginner card)

- Is there a path to upgrade without opening a new account?

- Does the APR matter? (Only if you plan to carry a balance — don’t)

How to Get Approved Fast: Step-by-Step

Getting approved for your first card isn’t complicated, but doing it wrong can hurt you before you start.

Step 1: Check pre-qualification tools first. Most major issuers — Capital One, Discover, Chase — offer soft-pull pre-qualification that doesn’t affect your credit score. Use these to see your odds before you apply.

Step 2: Apply only for cards designed for your credit level. Applying for a premium rewards card with no credit history guarantees a rejection and leaves a hard inquiry on your file.

Step 3: Have your documents ready. You’ll need: your Social Security Number (or ITIN for immigrants), proof of income (job, scholarships, or even regular allowances count), your address history, and your date of birth.

Step 4: Apply for one card at a time. A credit card application creates a hard inquiry on your credit report, which may temporarily lower your score by 5 to 10 points. This effect fades within 12 months. Apply for only one card at a time to minimize impact.

Step 5: Consider a secured card if rejected. If you’re denied for an unsecured card, a secured card with a $200 deposit is a guaranteed approval path. Six months of on-time payments will often qualify you for unsecured options.

Step 6: If you’re a student, use that status. Student cards like the Discover it® Student have lower credit requirements specifically because issuers value the long-term relationship with young customers.

How to Build Your Credit Score Fast in 2026

Getting the card is step one. What you do next determines how fast you climb.

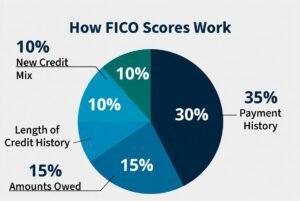

Your FICO score is calculated across five factors:

Payment history (35%): Whether you’ve paid past credit accounts on time. Amounts owed (30%): The amount of credit and loans you are using. Length of credit history (15%): How long you’ve had credit. New credit (10%): Frequency of credit inquiries and new account openings. Credit mix (10%): The variety of your credit accounts.

Here’s how to use that knowledge tactically:

Attack the 35% (payment history) first. Set up autopay for at least the minimum payment. One missed payment can sink your score by 50–100 points. Even one late payment stays on your report for up to seven years.

Control the 30% (amounts owed / utilization). Keep your balance below 30% of your credit limit at all times — ideally under 10%. If your limit is $500, never carry more than $150. Pay down the balance before your statement closes, not just the due date.

Start your 15% clock today. Every day your account is open, your credit age grows. Opening your first card as early as possible gives you the most time.

Use Experian Boost for free extra points. Tools like Experian Boost, RentTrack, Esusu, and certain property management systems allow consumers to report positive rent, utility, cellphone, and streaming payments to the credit bureaus — significantly improving credit scores for people with thin or no credit files.

Realistic timeline with responsible use:

| Timeframe | Expected Score Range |

|---|---|

| 0 months (no credit) | No score |

| 3 months | 600–640 (thin file) |

| 6 months | 640–680 |

| 12 months | 680–720 |

| 24 months | 720–760+ |

Results vary based on utilization and payment history — but these benchmarks are achievable for disciplined beginners.

Common Mistakes Beginners Make (Avoid These!)

You’ve gotten the card. Don’t blow it with these classic errors.

Mistake #1: Maxing out the card This is the single fastest way to destroy your score before it starts. Using $480 of a $500 limit pushes your utilization to 96% — a red flag to every credit scoring model in existence. Use the card for small recurring purchases. Think Netflix subscription and groceries, not furniture shopping sprees.

Mistake #2: Only paying the minimum The minimum payment is a trap. Pay the minimum, carry a balance at 27% APR, and your $500 balance becomes $635 in 12 months — and your utilization never improves. Pay in full every single month.

Mistake #3: Applying for multiple cards at once It feels logical: apply to five cards and pick the best offer. In reality, each application creates a hard inquiry. Five applications in one week looks desperate to lenders and can drop your score 25–50 points overnight.

Mistake #4: Closing the account after upgrading If you graduate from a secured card to an unsecured card, keep the old account open (with a $0 balance if possible). Closing it shrinks your available credit, spikes your utilization, and reduces your average account age.

Mistake #5: Ignoring your monthly statements Fraud happens to beginners more than anyone — partly because they don’t check. Log in weekly. Set up transaction alerts. Dispute anything unfamiliar within 60 days.

Mistake #6: Thinking your score doesn’t exist yet After 6 months with one active card, FICO generates your first score. Many beginners don’t check for months and miss the feedback they need to course-correct.

Pro Tips Used by Smart Americans

These are the habits that separate people who plateau at 680 from those who hit 750 in under two years.

The “one small purchase” strategy. Use your card for a single recurring charge — a streaming service, a phone bill, a weekly grocery run. Set autopay for the full balance. You’ll build credit on autopilot without ever worrying about debt.

Request a credit limit increase at 6 months. A higher limit with the same spending means lower utilization. Most issuers will grant a limit increase after 6 months of on-time payments — and many do it automatically. This single step can add 20–40 points to your score.

Pay twice a month. If you’re worried about utilization, make a payment in the middle of your billing cycle and another at the due date. This keeps your reported balance low even if you use the card frequently.

Become an authorized user. If a family member or close friend has a credit card in good standing (no late payments, low utilization), ask to be added as an authorized user. Their positive history can appear on your credit report immediately — without you even using the card.

Monitor with free tools. Every major issuer provides a free FICO score in their app. Capital One offers CreditWise, Discover provides a free FICO score monthly, and Chase has Credit Journey. Use them all. Knowledge is your best credit-building tool.

Don’t apply for anything new in the first year. Let your first account breathe. Every new application triggers a hard inquiry. Give your score 12 months to build cleanly before diversifying.

Frequently Asked Questions

What is the easiest credit card to get in the USA with no credit?

You can get a credit card with no credit score simply by choosing a credit card intended for beginners, filling out and submitting an online application, and then waiting. If you are 18+ years old and have enough income to afford the monthly bill payments, you stand a good chance of getting approved. The easiest options in 2026 are secured cards like the Discover it® Secured or Capital One Quicksilver Secured — both have no minimum credit score requirement.

Can I get a credit card with no credit history in the USA?

Yes. Just because you have no credit history doesn’t mean you can’t get a credit card. Some cards in this category are secured and require a cash deposit while others are designed for students. Using one of these cards responsibly can help you establish credit and, in some cases, even earn rewards.

What credit score do I need to get a beginner credit card?

For secured cards (Discover it® Secured, Capital One Quicksilver Secured), no credit score is required — you’re approved based on income and your security deposit. For unsecured beginner cards like Chase Freedom Rise℠ or Petal 2, having some income is typically sufficient even with zero credit history. For the Bank of America Customized Cash, a score of 670 or above is generally needed.

How fast can I build credit from scratch?

With responsible use, you can have a scoreable FICO file within 3–6 months of opening your first account. Most beginners can reach a “good” credit score (670+) within 12 to 18 months. Hitting 750+ realistically takes 24 months of consistent, disciplined use. The average FICO Score in the U.S. has climbed steadily over the years, partly because people have become much more aware of credit and how it works.

Is it better to start with a secured or unsecured card?

It depends on your situation. If you have zero credit history and are unsure about approval odds, a secured card is the safer, guaranteed path. If you have income and can qualify for an unsecured beginner card like Chase Freedom Rise℠ or Petal 2, the unsecured route saves you from tying up $200–$500 in a deposit. Both paths lead to the same destination — a strong credit profile — as long as you use the card responsibly.

Do student credit cards affect my credit score?

Yes — and positively, when used correctly. Student cards report to all three major credit bureaus (Experian, Equifax, and TransUnion) just like any other credit card. The Discover it® Student Cash Back is particularly strong because it has no annual fee, no credit history requirement, and the same Cashback Match promotion as the regular Discover it Secured.

The Bottom Line

Your first credit card is more than a piece of plastic. It’s your entry point to the U.S. financial system — and the first chapter of a credit story that will follow you for life.

In 2026, beginners have more options than ever. Whether you’re a student, an immigrant, or someone who simply never got around to building credit, there is a card on this list designed exactly for you. The Discover it® Secured Credit Card is the best overall pick for most beginners — zero annual fee, real cash back rewards, and a clear upgrade path. If you can’t spare a deposit, the Chase Freedom Rise℠ and Petal 2 Visa offer unsecured approval without requiring a credit history.

Pick one card. Use it for small purchases. Pay it in full every month. Check your score every 30 days. That’s the entire playbook — and it works.

Six months from now, the credit door that once felt permanently closed will start to open. One year from now, you’ll be eligible for cards that once seemed out of reach. Two years from now, you’ll have the credit score that changes what’s possible in your financial life.

The best time to start was yesterday. The second best time is right now.

Disclaimer: Card terms, APRs, and features are subject to change. Always verify current offers directly with the card issuer before applying. This article is for educational purposes and does not constitute financial advice.